One Website With Complete Online Registration.

StyleMyCatalog.in will help you to understand the registration process and prepare your proper documents so that you will able to register your business on GST Portal without any rejections.

Who will collect TCS under GST?

E-commerce aggregators are responsible under the GST law for collecting and depositing tax at the rate of 1% from each transaction. Any dealers/traders selling goods/services online would get the payment after deduction of 1% tax.

All the traders/dealers selling goods/services online would need to get registered under GST even if their turnover is less than 20 Lakhs for claiming the tax deducted by aggregators.

Note: Supplier of services, who is not supplying through an e-commerce operator liable to collect tax at source, having a turnover of less than 20 lakhs are exempted from obtaining registration under GST .

Who will deduct TDS under GST?

TDS is to be deducted at the rate of 1% on the payments made to the suppliers of taxable goods and/or services, where the total value of such supply, under an individual contract, exceeds Rs. 2,50,000.

The following people/entities need to deduct TDS:

- A department or establishment of the Central or State Government

- Local authorities

- Government agencies

- a. an authority or board or any other body :

i. set up by an Act of parliament or a state legislature or

ii. established by any government

with fifty-one percent or more participation by way of equity or control.

b. The society established by the central government or state government or any local authority

c. Public sector undertakings as notified in the latest notification dated 13th Sep 2018.

Registration

Any person who is required to deduct TDS or collect TCS will electronically submit an application for registration, duly signed or verified through EVC (electronic verification code), using the FORM GST REG-07 on the Common Portal; either directly or from a Facilitation Centre notified by the Commissioner

The proper officer will grant registration after verification and issue a certificate of registration in FORM GST REG-06 within 3 working days from the date of submission of application

Cancellation of Registration

- If the proper officer enquires or ascertains through a proceeding that a person is no longer liable to deduct TDS or collect TCS, then the officer will cancel the registration. The cancellation shall be communicated to the said person electronically in FORM GST REG-08

- The officer will follow the same procedure for cancellation as for normal taxpayers

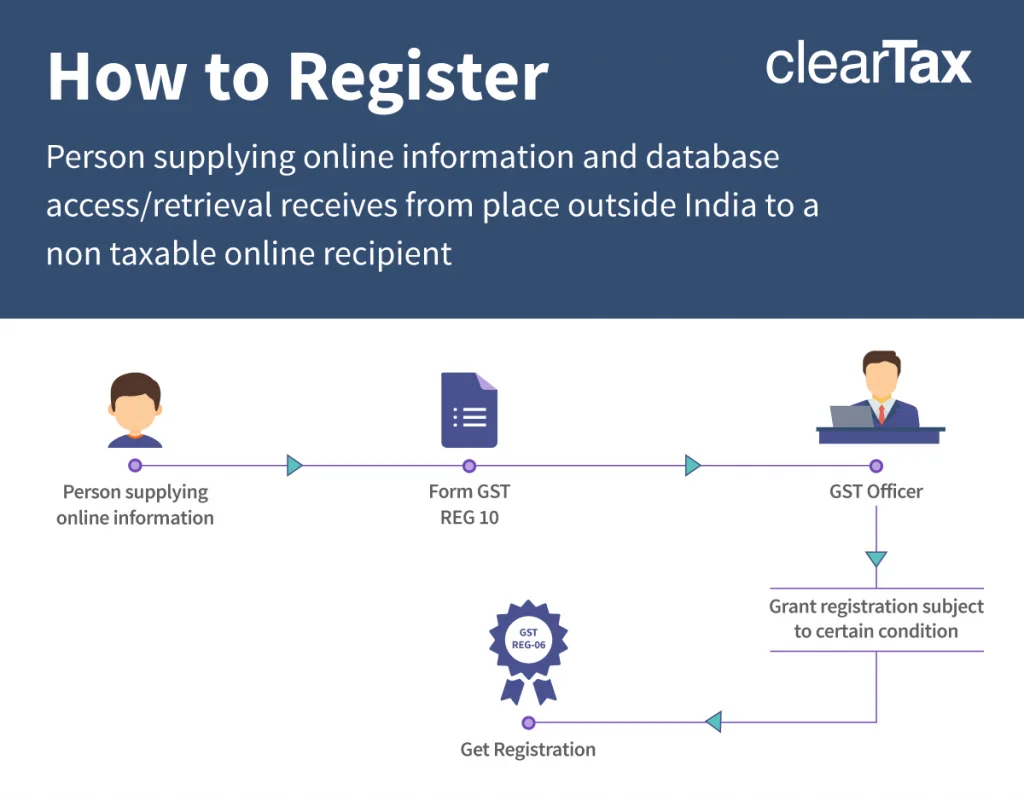

Registration for People Supplying Online Information from Outside India

What does online information and database access or retrieval services mean?

Online information and database access or retrieval services [OIDAR] means services whose delivery is mediated through the internet. The supply is essentially automated involving minimal human intervention and impossible without information technology.

On whom will this apply?

These are a few examples of electronic services from the service tax list which will be considered as OIDAR-

- Advertising on internet

- Providing cloud services (Google Drive)

- Provision of e-books, movie, music, software and other intangibles via internet (Hotstar, Amazon Prime Video)

- Providing data or information, retrievable or otherwise, to any person, in electronic form through a computer network

- Online gaming (Steam)

- Web-based services providing trade statistics, legal and financial data, matrimonial services, social networking sites etc

Non-OIDAR services

- Supplies of goods, where the order and processing is done electronically

- Supplies of physical books, newsletters, newspapers or journals

- Services of lawyers and financial consultants who advise clients through email

- Booking services or tickets to entertainment events, hotel accommodation or car hire

- Educational or professional courses, where the content is delivered by a teacher over the internet

- Offline physical repair services of computer equipment

- Repair of software, or of hardware, through the internet, from a remote location

- Advertising services in newspapers, on posters and on television

- Internet backbone services and internet access services (BSNL broadband)

It has also been clarified that using the internet just to communicate or facilitate outcome of service need does not always mean that a business is providing OIDAR services.

Registration Process

Here’s a link to download the government of India prescribed GST registration form.

GST Registration for e-Commerce Collecting TCS under GST

Irrespective of sectors, GST has a noticeable impact on each and every business. e-Commerce sector is also not an exception. Registration under GST is mandatory for all e-commerce operators irrespective of the sales turnover. Within 30 days of commencing business, an e-commerce operator is required to get registered under GST.

There can be two types of e-commerce sellers:

- e-Commerce operators like Flipkart and Amazon; an entity that owns, operates or manages digital platform for e-commerce.

- e-Commerce suppliers; an entity that supplies goods or services on a digital e-commerce platform.

Table of Content

- Collection of Tax at Source (TCS)

- Process of GST registration for e-commerce

- Insights on GST TCS

- TCS compliance for e-commerce sector

Provisions of Section 52: Collection of Tax at Source (TCS)

Section 52 is only applicable for ecommerce operators. According to the section:

- An ecommerce operator needs to collect tax @1% from the supplier This shall be done by the Operator by paying the supplier, the price of the product/services, less the tax, calculated at the rate of 1%.

- Such withheld amount is to be deposited as TCS by the 10th of the next month.

- The deposited TCS amount will reflect in the electronic cash ledger of the supplier.

- This ledger reflects the entire deposits made in cash, and TDS/TCS made on account of the taxpayer on real time basis. And information appearing in this ledger can be utilised for making any payment on account of GST.

Note: Similar to TDS, TCS (Tax Collection at Source) is a mechanism under GST. Here, the ecommerce operator collects a portion of tax from the supplier at the time of supply of goods/services.

Process of GST Registration for e-Commerce

- Any person who is required to collect TCS will fill the application for registration in FORM GST REG-07 and submit it electronically, either directly or from a Facilitation Centre notified by the Commissioner.

- The proper officer will grant registration after verification and issue a certificate of registration in FORM GST REG-06 within 3 working days from the date of submission of application.

Insights on GST TCS

- All the businesses that are supplying services through an ecommerce platform will be liable for TCS.

- When ecommerce suppliers store their goods at a common warehouse, they must include the details of warehouse as a business place while registering for GST.

- The calculation and deduction rate of TCS is 1% of the net value of the goods or services supplied through the ecommerce operator.

For instance, a supplier sells his product worth INR 50,000 through Amazon. The entire amount would be collected by Amazon. This revenue would be transferred to the supplier by Amazon after deducting 1% tax (i.e. INR 500), which is called TCS. This 1% TCS would be remitted to the government. The TCS (INR 500) remitted by the ecommerce operator will be provided as credit to the supplier. - The amount collected by an ecommerce operator as GST TCS must be remitted with the Government before 10 days after the end of the month in which the particular amount was collected.

- The amount which an ecommerce operator deducts as of TCS and remits to the Government is treated as credit while filing GSTR-2 return. Further, at the time of filing GSTR-3 or GSTR-3B return, this can be used to set-off the liability of GST.

- It is mandatory to file GSTR-8 on monthly basis by the 10th of the next month, and annual return by 31st December following the end of every financial year. It is must to include details of outward supplies made by sellers through ecommerce platform and the amount collected as TCS.

Insights on GST TCS

- All the businesses that are supplying services through an ecommerce platform will be liable for TCS.

- When ecommerce suppliers store their goods at a common warehouse, they must include the details of warehouse as a business place while registering for GST.

- The calculation and deduction rate of TCS is 1% of the net value of the goods or services supplied through the ecommerce operator.

For instance, a supplier sells his product worth INR 50,000 through Amazon. The entire amount would be collected by Amazon. This revenue would be transferred to the supplier by Amazon after deducting 1% tax (i.e. INR 500), which is called TCS. This 1% TCS would be remitted to the government. The TCS (INR 500) remitted by the ecommerce operator will be provided as credit to the supplier. - The amount collected by an ecommerce operator as GST TCS must be remitted with the Government before 10 days after the end of the month in which the particular amount was collected.

- The amount which an ecommerce operator deducts as of TCS and remits to the Government is treated as credit while filing GSTR-2 return. Further, at the time of filing GSTR-3 or GSTR-3B return, this can be used to set-off the liability of GST.

- It is mandatory to file GSTR-8 on monthly basis by the 10th of the next month, and annual return by 31st December following the end of every financial year. It is must to include details of outward supplies made by sellers through ecommerce platform and the amount collected as TCS.

GST Registration For Company ![]() | @ Rs 299/-INR ONLY -Online.

| @ Rs 299/-INR ONLY -Online.

GST No objection certificate from landlord  | @ Rs 199/-INR ONLY -Online.

| @ Rs 199/-INR ONLY -Online.

Have you Filed your GST Returns Yet?

Our experts at StyleMyCatalog can help you file all your GST returns and help you with GST compliance. Get your GST returns filed now!

Find Us On Twitter!  For Batter Understanding.

For Batter Understanding.

Find Us On Facebook! ![]() For Batter Understanding.

For Batter Understanding.

For a free consultation regarding your e-commerce website. Get in touch with us. Contact us!